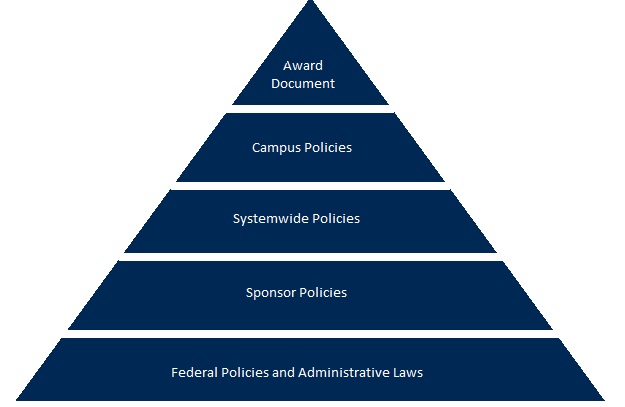

There are many levels of guidance one must consider when managing awards. When policies differ, follow the most restrictive rule. Click on the links to your right to learn more about the various policies that govern awards.